For decades, supercomputing was the domain of physics, engineering, and national research labs. Now, the focus has shifted to GPUs, and for the first time, the financial sector is looking to trade GPU compute capacity just as it does oil, electricity, and agricultural commodities.

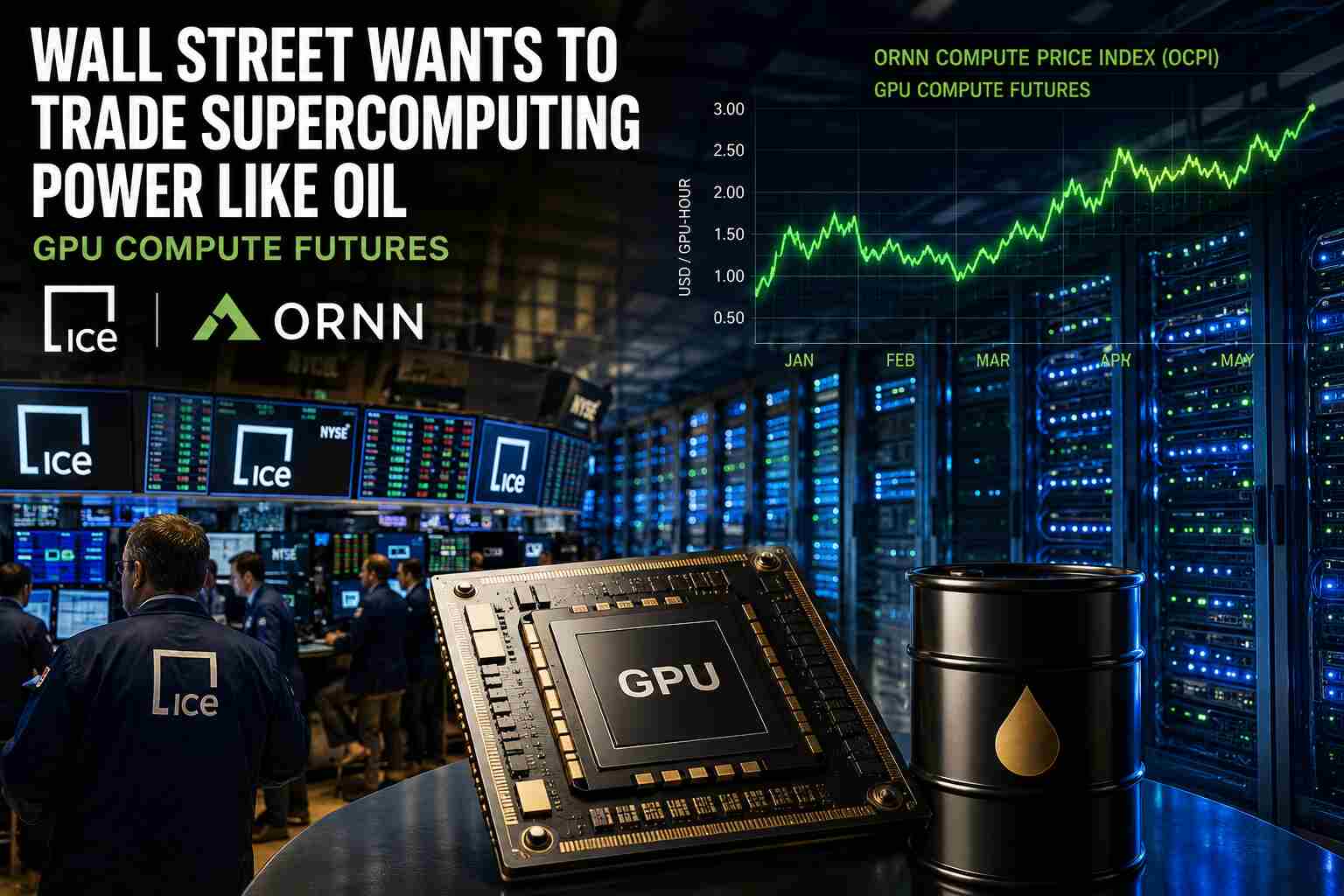

This week, Intercontinental Exchange (ICE) and Ornn announced plans to launch GPU compute futures contracts tied to Ornn’s Compute Price Index (OCPI), a benchmark designed to track the market price of AI compute infrastructure. The move may sound like a niche financial experiment, but its implications for the supercomputing industry are enormous.

The era of compute as a commodity has arrived.

According to the announcement, the futures contracts are intended to help AI companies, hyperscalers, cloud providers, and datacenter operators hedge against the increasingly volatile cost of GPU resources.

That volatility has become one of the defining economic realities of modern high-performance computing.

Over the past three years, demand for NVIDIA accelerators such as the H100, H200, and Blackwell-class GPUs has made compute infrastructure a scarce strategic resource. AI labs are spending billions assembling clusters with tens of thousands of GPUs. Cloud providers now ration accelerator access. Entire data center projects are being financed based on projected AI compute demand rather than on traditional enterprise workloads.

The result is that GPU pricing no longer behaves like conventional server hardware pricing. It behaves more like an energy market.

That distinction matters.

Commodity futures markets emerge when industries become too economically dependent on volatile supply and pricing. Airlines hedge jet fuel. Utilities hedge electricity. Farmers hedge grain prices. Now the AI sector appears ready to hedge compute itself.

The significance for supercomputing is difficult to overstate.

Historically, HPC procurement cycles were relatively predictable. National laboratories and research institutions purchased systems every several years through long planning horizons. But AI supercomputing has compressed infrastructure demand into a chaotic global race. A single delay in GPU availability can derail billion-dollar training schedules.

In that environment, financial hedging starts to look less speculative and more operationally necessary.

The ICE-Ornn initiative also reveals how dramatically AI infrastructure has altered the perception of computing resources. GPUs are no longer simply components inside a machine. They are becoming financial assets with measurable market exposure.

That evolution mirrors another major industry shift unfolding in parallel: the rise of “AI factories.” Companies increasingly describe hyperscale GPU clusters not as datacenters, but as production infrastructure designed to manufacture intelligence. Once computing becomes industrial production capacity, financial markets inevitably follow.

And ICE is not alone in seeing the opportunity.

Just last week, CME Group announced its own partnership aimed at launching compute futures products, suggesting a broader race is underway to establish the financial plumbing of the AI economy. What once sounded futuristic is rapidly becoming institutionalized. Computing derivatives may soon become a standard feature of enterprise AI operations.

Still, the concept raises difficult questions.

Unlike oil or electricity, GPU compute is not perfectly standardized. Performance varies dramatically depending on interconnects, memory bandwidth, software stacks, cooling efficiency, networking architecture, and workload optimization. A Blackwell GPU inside a tightly optimized liquid-cooled AI supercluster is not economically equivalent to a standalone accelerator sitting in a conventional cloud instance.

That creates a fundamental challenge for any compute futures market: can AI compute truly be reduced to a fungible commodity?

There is also the risk that financialization itself could worsen volatility. Commodity markets do not merely stabilize industries; they also attract speculation. Hedge funds and institutional traders entering compute markets could introduce entirely new pricing distortions into already constrained GPU supply chains.

For research institutions and smaller HPC centers, that prospect is concerning. Wealthy hyperscalers already dominate global GPU acquisition. If compute markets become financial instruments, access to advanced accelerators may become even more detached from scientific priorities and increasingly driven by market dynamics.

Yet the direction of travel appears unmistakable.

The supercomputing industry is no longer just building machines. It is building an economy around computing itself.

For years, HPC experts warned that AI would transform datacenter architecture, energy infrastructure, networking, and semiconductor design. What few anticipated was that it would also transform Wall Street.

Now the financial sector wants a stake in the world’s most valuable resource: compute.