For decades, the supercomputing industry treated memory as a supporting technology, important, expensive, but ultimately secondary to processors. That hierarchy is now collapsing.

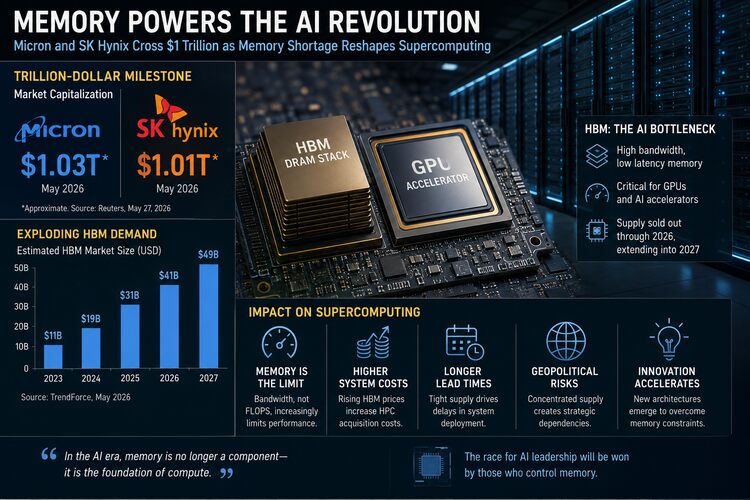

In a remarkable shift driven by the global artificial intelligence infrastructure race, memory manufacturers Micron Technology and SK Hynix have both surpassed $1 trillion in market capitalization, joining an elite tier once dominated almost exclusively by software giants, hyperscalers, and CPU designers.

The catalyst is not traditional DRAM demand from PCs or smartphones. It is the emergence of high-bandwidth memory (HBM) as the critical bottleneck in AI supercomputing systems.

In effect, the industry has discovered that compute acceleration without memory bandwidth is useless.

The memory crisis behind the AI boom

Modern AI supercomputers depend on massive parallel data movement. GPUs can perform extraordinary numbers of floating-point operations, but only if memory subsystems can continuously feed them data at sufficient speed.

That requirement has transformed HBM from a niche premium technology into the most strategically important component in the AI supply chain.

HBM stacks DRAM vertically and places it in close proximity to accelerators such as GPUs and AI ASICs, dramatically increasing memory bandwidth while reducing latency and power consumption. NVIDIA’s latest AI systems, for example, rely heavily on HBM capacity supplied primarily by Micron, SK Hynix, and Samsung Electronics.

The result is a structural supply shortage unlike previous semiconductor cycles.

Industry reports indicate that HBM production capacity is effectively sold out through 2026, with some supply commitments extending into 2027.

This shortage is now reshaping the economics of the entire HPC ecosystem.

Why is this different from previous memory cycles

Historically, memory markets were notoriously cyclical. Oversupply repeatedly crushed DRAM pricing, destroying margins and valuations.

Investors treated memory vendors as commodity manufacturers.

AI infrastructure is changing that assumption.

HBM manufacturing is vastly more complex than commodity DRAM. Advanced packaging, thermal constraints, TSV stacking, and proximity integration with accelerators create production limitations that cannot be expanded quickly. Each HBM stack also consumes substantially more wafer capacity than standard DRAM products.

This means supply elasticity has weakened precisely as demand has exploded.

The market is increasingly pricing memory manufacturers not as cyclical commodity vendors, but as strategic infrastructure gatekeepers. Reddit investor discussions, often an early indicator of broader retail sentiment, increasingly describe HBM suppliers as occupying “the AI toll booth.”

That language would have been unthinkable in semiconductor markets only three years ago.

The implications for supercomputing

For the supercomputing industry, the implications are profound.

1. Memory bandwidth is becoming the primary scaling constraint

Traditional HPC procurement focused primarily on FLOPS and interconnect performance. Increasingly, however, system architects are discovering that AI and exascale workloads are memory-bound rather than compute-bound.

Large language models, graph analytics, molecular simulation, weather forecasting, and multimodal AI systems all require enormous memory throughput.

This changes procurement priorities.

Future leadership-class supercomputers may be differentiated less by raw compute density and more by memory subsystem architecture and access efficiency.

The industry’s center of gravity is moving from processor-centric design toward memory-centric system engineering.

2. Supercomputer costs will rise

Persistent HBM shortages are already driving dramatic price increases in memory components.

Reuters reported memory pricing doubled in the first quarter of 2026, with further increases expected.

For HPC operators, this translates directly into higher system acquisition costs.

National laboratories, cloud providers, and enterprise AI operators may increasingly compete for the same limited pool of memory resources. That competition risks extending procurement lead times and delaying deployment schedules for new supercomputing systems.

In practical terms, memory may become the pacing factor for global AI infrastructure deployment.

3. The industry’s power structure is changing

For years, the semiconductor hierarchy revolved around CPU vendors and, later, GPU manufacturers.

Now, memory vendors are becoming strategic equals.

This is particularly important because the HBM market is highly concentrated. Micron, SK Hynix, and Samsung collectively dominate advanced memory production.

Such concentration introduces geopolitical and supply chain risk into the supercomputing ecosystem.

The United States increasingly views Micron as a strategic domestic supplier, while South Korea’s memory industry has become central to global AI infrastructure economics.

Future export controls, trade disputes, or manufacturing disruptions could therefore impact AI supercomputing capacity worldwide.

4. HPC architecture innovation will accelerate

The memory shortage is also likely to accelerate architectural innovation.

Researchers and vendors are already exploring:

- Near-memory computing

- Processing-in-memory architectures

- CXL-based memory pooling

- Optical interconnects

- Advanced caching hierarchies

- HBM alternatives and hybrid memory systems

The economics of memory scarcity will force the industry to become more efficient in data movement and memory utilization.

That could ultimately reshape software design as much as hardware engineering.

A warning sign for the AI infrastructure economy

There is, however, another way to interpret these trillion-dollar valuations.

They reflect not just technological progress, but also expose a new vulnerability in the AI ecosystem.

The AI industry now relies heavily on a handful of companies that can produce the advanced memory needed for cutting-edge accelerators. If memory supplies remain tight through 2027, as some industry leaders predict, the growth of AI infrastructure could stall regardless of GPU availability.

In this context, the soaring valuations of Micron and SK Hynix signal not just success, but the emergence of a new bottleneck for AI supercomputing.

While computing scarcity once dominated industry concerns, it is now clear that memory shortages could prove even more critical.